Calculate Your Home Loan Payments: An Easy Step-by-Step Guide

Understanding your future financial obligations is paramount when considering a home loan. Indeed, knowing how to calculate your home loan payments empowers you to budget effectively and make informed decisions. This easy guide will walk you through the process, providing clarity and real-world examples.

Why Understanding Your EMI is Crucial

Being able to calculate home loan payments before you commit to a loan offers several key benefits. Firstly, it allows for effective budgeting, enabling you to determine if the monthly payments fit comfortably within your financial constraints. Secondly, you can use these calculations for comparing loan options, evaluating different loan amounts, interest rates, and tenures to see their impact on your monthly outgo. Furthermore, understanding the calculations can give you more confidence during negotiation with lenders regarding loan terms. Finally, it aids in long-term planning, helping you visualize the total cost of the loan over its entire tenure.

Key Factors Influencing Your Home Loan Payments

To accurately calculate your home loan payments, you need to understand these key components. Primarily, there’s the Principal Loan Amount (P), which is the initial sum you borrow. Next is the Annual Interest Rate (r), the percentage charged by the lender per year. Lastly, we have the Loan Tenure (n), which is the duration of the loan, typically expressed in months.

The Essential Formula for Calculating Your EMI

The most common method to calculate home loan payments involves using the Equated Monthly Installment (EMI) formula:

qquadEMI=Ptimesfracr(<0>1+r)n(1+r)n−1

Where:

- EMI = Equated Monthly Installment

- P = Principal Loan Amount

- r = Monthly interest rate (Annual interest rate / 12)

- n = Loan tenure in months

Step-by-Step Guide to Manual Calculation

While the formula might initially seem intimidating, you can easily calculate your home loan payments by following these steps. First, determine the Principal Loan Amount (P). For example, if the property costs ₹60,00,000 and you make a down payment of ₹15,00,000, your principal loan amount becomes ₹45,00,000. Second, find the Annual Interest Rate, which will be provided by your lender. Let’s assume it’s 9% per annum. Third, calculate the Monthly Interest Rate (r) by dividing the annual interest rate by 12. In our example, r = 9% / 12 = 0.09 / 12 = 0.0075. Fourth, determine the Loan Tenure in Months (n). If your loan tenure is 20 years, then n = 20 years × 12 months/year = 240 months. Finally, plug the values into the EMI Formula:

qquadEMI=45,00,000timesfrac0.0075(1+0.0075)240(1+0.0075)240−1

qquadEMIapprox₹40,475.77

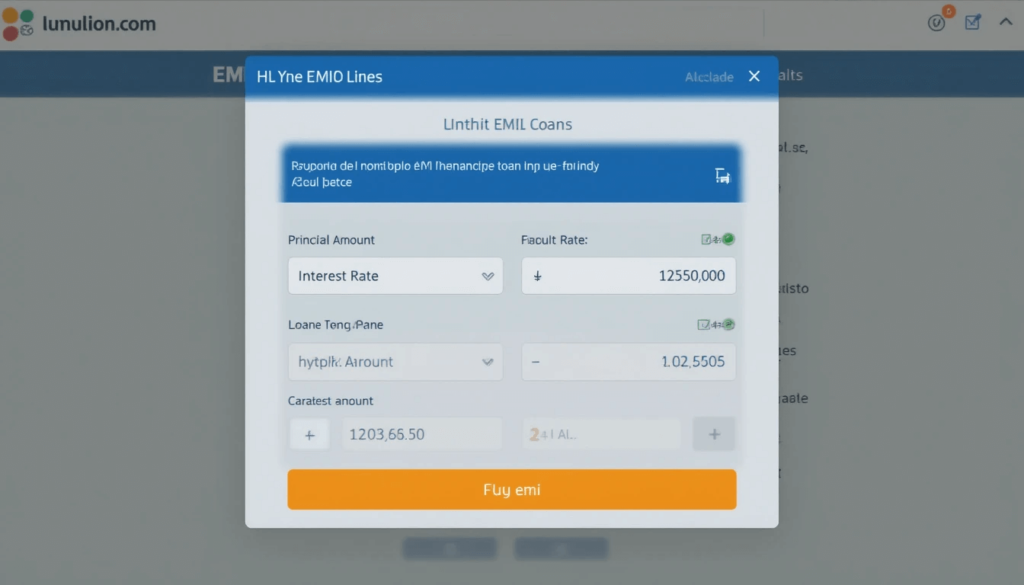

The Convenience of Online EMI Calculators

Fortunately, the easiest way to calculate your home loan payments is by using online EMI calculators provided by various banks and financial institutions. These tools are remarkably user-friendly; you simply input the principal amount, interest rate, and loan tenure to get the EMI instantly.

Real-World Application: Priya’s Home Loan

Consider Priya, who is looking to buy a house and needs a loan of ₹30,00,000. She has found a lender offering an 8.5% annual interest rate for a 15-year loan tenure. By using an online home loan EMI calculator, she can quickly determine her monthly payment:

- Principal Loan Amount (P): ₹30,00,000

- Annual Interest Rate: 8.5%

- Loan Tenure: 15 years (180 months)

The online calculator shows her estimated monthly EMI to be approximately ₹29,563.

Key Takeaways for Effective Home Loan Planning

In conclusion, remember these actionable takeaways. Firstly, always calculate your home loan payments before finalizing a loan agreement. Secondly, utilize online EMI calculators for quick and accurate results. Thirdly, experiment with different loan amounts, interest rates, and tenures to fully understand their impact on your monthly payments. Lastly, don’t forget to factor in other potential costs such as property taxes and insurance when budgeting for your home loan.

")

{kind=link}